Foram encontradas 371 questões.

Uma empresa fabricante de chuteiras de futebol com poder de mercado tem curva de demanda inversa para o seu produto dada por P = 110 - 20Q, em que P é o preço em reais e Q é a quantidade em mil chuteiras. A empresa possui custo marginal dado por CMg = 10 + 10Q. Julgue o item a seguir:

Item 1 - Se a empresa tiver a capacidade de praticar a discriminação perfeita de preços, ela produzirá 3,33 mil chuteiras.

Provas

Questão presente nas seguintes provas

Comparando-se os dois principais ciclos expansivos da economia brasileira (1º: 1956-1961 – 2º: 1967-1973), é correto afirmar:

Item 1 - No segundo ciclo o coeficiente de importações em relação ao PIB aumentou significativamente em relação ao primeiro ciclo, portanto a estabelecer contraste pela acentuada abertura estrutural para o exterior no segundo ciclo em relação ao primeiro ciclo.

Provas

Questão presente nas seguintes provas

Julgue a veracidade da seguinte afirmativa:

Item 1 - A matriz !$ A !$ !$ \begin{bmatrix} \dfrac{1}{2} & 1 & 4 \\ 0 & -\dfrac{1}{2} & 3 \\ 0 & -\dfrac{1}{2} & 2\end{bmatrix} !$ é diagonalizável.

Provas

Questão presente nas seguintes provas

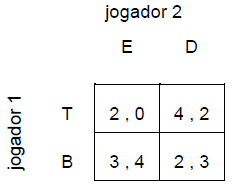

Com relação à Teoria dos Jogos, julgue o item a seguir:

Item 2 - No Equilíbrio de Nash em estratégias mistas do jogo abaixo, o jogador-1 joga T com probabilidade 1/3 e B com probabilidade 2/3, ao passo que o jogador-2 joga E com probabilidade 2/3 e D com probabilidade 1/3:

Provas

Questão presente nas seguintes provas

Sobre a economia cafeeira na Primeira República e no início da Era Vargas (1930-1945), é correto afirmar:

Item 0 - Na última década do século XIX, um conjunto de fatores impulsionou a expansão da cafeicultura, como a crise da oferta de café colombiano no mercado internacional, como o crescimento da oferta de mão de obra nacional nas fazendas de café, e como o crescimento do financiamento externo para a abertura de novas terras para o cultivo.

Provas

Questão presente nas seguintes provas

Com relação às interpretações teóricas que marcaram a história do pensamento econômico brasileiro, pode-se afirmar:

Item 3 - Os economistas de tradição cepalina defenderam que a economia agroexportadora vigente antes de 1930 era marcada pelo dualismo estrutural, e que após 1930, com a industrialização por substituição de importações, a dualidade seria superada.

Provas

Questão presente nas seguintes provas

Sobre as iniciativas de política econômica e os resultados da abertura comercial da década de 1990, pode-se afirmar:

Item 3 -As transformações na estrutura produtiva alteraram a inserção externa da indústria brasileira: as importações tornaram-se superiores às exportações nos segmentos de bens de consumo e bens intermediários simples, e as exportações tornaram-se superiores às importações nos segmentos de bens de capital e insumos elaborados.

Provas

Questão presente nas seguintes provas

Seja !$ p^i_t !$ o preço do bem i no período t, e seja !$ q^i_t !$ a quantidade vendida do bem i no período t. Considerando dois bens (i = 1, 2) e dois períodos (t = 1, 2), verifique se a afirmativa abaixo está correta, supondo que !$ p^1_1 < p^1_2 ,p^2_1 < p^2_2, q^1_1 > q^1_2, q^2_1 > q^2_2 !$:

Item 2 - O Índice de Preço de Laspeyres do período 2 com base no período 1 é dado por:

!$ \dfrac{r^1v^1_2+r^2v^2_2}{v^1_1+v^2_1} !$

em que !$ v^i_t=p^i_t q^i_t !$ e !$ r^i=p^i_2/p^i_1 !$.

Provas

Questão presente nas seguintes provas

Seja a função !$ f:\mathbb{R}^2\rightarrow \mathbb{R} !$ definida por !$ f(x_1,x_2)=e^{100x_1-5x^2_1+40x_2-5x^2_2+3} !$. Se !$ D((x_1,x_2),(5,2)) !$ denota a distância euclidiana do ponto !$ (x_1,x_2) !$ ao ponto !$ (5,2) !$, e !$ \alpha \in \mathbb{R} !$ é um parâmetro, considere o problema P: maximizar !$ f(x)=f(x_1,x_2) !$ em !$ x=(x_1,x_2)\in \mathbb{R}^2 !$ sujeito à restrição !$ D((x_1,x_2),(5,2) \le \alpha !$. Julgue a seguinte afirmativa:

Item 4 - A função !$ g !$ sobre !$ \mathbb{R}^2 !$ definida por !$ g(x_1,x_2)=lnf(x_1,x_2) !$ é côncava.

Provas

Questão presente nas seguintes provas

Printing money is valid response to coronavirus crisis

Quantitative easing programmes may be here for the long term

Financial Times Editorial Board

APRIL 6 2020

https://www.ft.com/content/fd1d35c4-7804-11ea-9840-1b8019d9a987

The British government has never paid off the £1,200,000 loan that created the Bank of England in 1694. In exchange it gave the merchants who provided the money the exclusive right to print banknotes against this debt, giving birth to the central bank and much of the architecture behind the world’s financial system. Today, as policymakers promise to do “whatever it takes” to prop up their economies in the face of coronavirus, central banks are facing calls to print money to finance government spending directly.

In times of emergency, particularly war, central banks have often handed freshly printed banknotes to governments. The fight against resultant inflation was postponed until after any crisis. Despite the pandemic, the world is not yet in that position today. There is no need, for now, to relax the framework of independent, inflation-targeting central banking. Yet this kind of monetary financing should be a tool available to policymakers, if needed.

Without limits, allowing a government to finance itself by creating money can lead to hyperinflation. But these risks can be manageable: the quantitative easing of the past decade, despite predictions, has not lifted inflation above the main central banks’ 2 per cent targets. The money pumped into rich-world economies has been met by increased demand, perhaps permanently, for precautionary saving.

There is no clear distinction between quantitative easing and monetary financing. Central bankers say asset purchases under QE are temporary, meaning the newly-created money will one day be removed from the economy. But it is hard to bind the hands of their successors, who could one day make them permanent. Either way, the effect is to lower the cost of government borrowing. Buying the bonds only after they have been sold to private investors still frees up funds for new issues.

Recent QE programmes, in fact, look increasingly likely to become permanent. Central bankers were unable to complete a much-discussed programme of “normalising” monetary policy between the financial crisis and today’s crash. They are not going to be able to do so any time soon. The scale of previous schemes means the Bank of Japan — which holds government bonds worth more than 100 per cent of Japanese national income — may never be able fully to unwind its purchases.

The difference between QE and direct monetary financing is mostly one of presentation: whether asset purchases are deemed temporary or permanent. This matters: credibility and messaging are important features of central banking. An opinion article this week by Andrew Bailey, the Bank of England governor, that ruled out monetary financing may have been largely conceived to convince international investors that there is little reason to fear keeping funds in sterling.

If trends restraining inflation go into reverse, central bankers have tools to combat rising prices, whether through raising interest rates or unwinding QE. The present crisis may even be deflationary and central banks’ targets are, with the exception of the European Central Bank, symmetric in promising to tackle inflation that is both below and above their stated goal.

The scale of today’s downturn means even the most direct monetary financing, such as “helicopter money”, or handing cash to the public, should remain an option. This will require co-ordination with democratically elected officials, who are responsible for the public finances. The debate should not be over whether monetary financing can happen — in QE, it already is — but over keeping the process under control via independent central banks.

From the text we can infer that:

Item 1 - It is impossible to manage the risk of hyperinflation;

Provas

Questão presente nas seguintes provas

Cadernos

Caderno Container