Foram encontradas 400 questões.

Indique se a proposição, relativa às teorias do consumo e do investimento, está certo ou errado:

Item 4 - Ceteris paribus, uma queda na cotação das ações cotadas na Bolsa de Valores reduziria o chamado “q” de Tobin.

Provas

BASED ON YOUR INTERPRETATION OF THE TEXT THAT FOLLOWS, DETERMINE IF EVERY STATEMENT IS RIGHT OR WRONG.

THIRD TEXT

As dramatic as it was, the global financial crises of 1997-99 was only the most recent of a rash of crises that have devastated market economies over the last 25 years. By one calculation almost 100 countries experienced a severe currency or financial crisis during that period, with adverse consequences for their national budgets and economic growth. Such patterns clearly call for an explanation: although there has been no dearth of suggestions, a consensus is growing that at least part of the explanation lies in weak financial institutions, which result in part from inadequate government regulation. The pendulum has come full circle: from the burst of enthusiasm over deregulation, policymakers now appreciate why it is that the most successful economies have long had a strong tradition of financial regulation. In the Unites States financial regulation dates back to 1863, in the middle of the American Civil War, when it became apparent that a strong banking system was essential to create a new national economy and that such a system required a strong national regulatory structure. The most recent major lapse in regulation, the deregulation effort that began in 1981, led to the savings and loan debacle. The consequences of that crisis were so severe that the U.S. economy did not recover for close to a decade.

But many developing countries are struggling with precisely the opposite problem – an overregulated financial system that stifles innovation and the flow of credit to new entrepreneurs, stunting the growth of even well-established firms. One of the many adverse effects of the East Asian financial crisis is that countries have become wary of reforms that affect the financial sector, aware that they may leave the country worse off. This article argues that reforms are possible – and indeed needed – and can be undertaken without undue fear, but success requires understanding the basic principles of financial sector regulation. The article sets forth those principles.

Even before the crisis, a theoretical literature argued that the nature of financial market failures necessitated a strong role for government. Failures in the banking system have strong spillovers, or externalities, that reach well beyond the individuals and firms directly involved. To avoid a financial collapse, governments typically bail out the affected entity, whether or not formal deposit insurance is in place; this intervention itself gives rise to problems of moral hazard. Although the absence of formal deposit insurance might give depositors a slightly increased incentive to monitor financial institutions (because there is some uncertainty about whether they will actually be bailed out), individual monitoring is actually inefficient. Monitoring is a public good, and it needs to be publicly provided. Of course, at a more practical level, a small depositor cannot be expected to examine the books of a bank on a weekly basis; there is strong evidence that regulators and rating agencies have difficulties doing so. Indeed, the widespread misconceptions about the appropriate strategy for regulating the financial sector suggests that even so-called experts are not fully aware of some of the key issues. Why, then, should one expect more from an individual depositor with little training, interest, or capacity in the arcane details of financial accounting?

Despite its long history, financial market regulation is poorly understood, as evidenced by the disasters associate with deregulation in industrial and developing countries. Often such measures were pushed through a burst of enthusiasm for free markets without recognizing the inherent market failures associate with such markets. Today few economists advocate unregulated banking, but a similar ideological agenda has pushed excessive reliance on a single regulatory instrument – capital adequacy standards. The belief is that this measure entails the minimal interference with the workings of the market and avoids the well-recognized problems of unregulated banks. A deeper analysis of the financial sector, however, shows that such reliance is not only inefficient but may even be counterproductive under some circumstances.

Principles of Financial Regulation: A Dynamic Portfolio Approach. Joseph E. Stiglitz. The World Bank

Research Observer, vol. 16, nº 1, Spring 2001.

According to the text:

Item 4 - The essay’s key issue is not whether financial markets should be regulated but how the regulation should be carried out.

Provas

Considere uma economia com dois períodos na qual existem dois tipos de empresas de tecnologia: 50% são empresas do tipo A e 50% do tipo B, ambas necessitando de financiamento de $50. Empresas que não obtêm financiamento encerram suas atividades tendo valor zero. As empresas do tipo A no segundo período poderão valer $50 ou $80 (ambos com a mesma probabilidade), enquanto as empresas do tipo B poderão valer zero ou $120 (ambos com a mesma probabilidade). Nesta economia existe apenas um banco que capta recursos a uma taxa de 10%. O banco pode emprestar recursos às empresas, cobrando juros que serão pagos apenas no segundo período, caso o valor realizado da empresa seja suficientemente elevado. No caso de uma empresa do tipo A, por exemplo, ela somente pagará $50 se esse for seu valor realizado, independentemente da taxa de juros acordada. Já no caso de uma empresa do tipo B, não haverá pagamento algum se o valor realizado for zero. Finalmente, assuma que uma empresa não tomará um empréstimo que não possa pagar nem mesmo quando seu valor realizado for elevado.

Item 0 - Supondo que o banco pode distinguir os dois tipos de empresas, as taxas de juros mínimas que poderia cobrar das empresas do tipo A e B são respectivamente 20% e 120%.

Provas

Assinale C (certo) ou E (errado):

Item 3 - Se !$ X = (-1,1), Y = \Re \ e \ f : X \rightarrow Y : x \rightarrow f(x) = { \large x \over 1 - |x|} !$, então !$ f !$ é bijetiva.

Provas

Uma das características do desenvolvimento do capitalismo no Brasil diz respeito ao papel do Estado como fator de estímulo à industrialização. Esse papel foi exercido por meio de políticas fiscais e monetárias, de controle do mercado de trabalho e do provimemto de bens públicos. Assim, é correto afirmar que as razões que levaram o Estado a promover a industrialização do Brasil foram:

Item 2 - Os grandes projetos industriais têm fortes dificuldades para contornar problemas de capacidade ociosa e de balanço de pagamentos, exigências de infra-estrutura e dificuldades de suprimento de matérias-primas básicas.

Provas

Considere um investidor cuja composição da carteira é formada por dois ativos A e B.

Item 2 - Supondo-se que os retornos de A e B tenham a mesma variância, a diversificação dessa carteira nestes dois ativos somente reduzirá o risco total se o coeficiente de correlação entre os respectivos retornos for negativo.

Provas

BASED ON YOUR INTERPRETATION OF THE TEXT THAT FOLLOWS, DETERMINE IF EVERY STATEMENT IS RIGHT OR WRONG.

FIRST TEXT

At length, in 1776, our illustrious countryman, Adam Smith, published the “Wealth of Nations” – a work which has done for Political Economy what the Essay of Locke did for the philosophy of mind. In this work, the science was, for the first time, treated in its fullest extent; and the fundamental principles on which the production of wealth depends, established beyond the reach of cavil and dispute. In opposition to the Economists, Dr. Smith has shown that labor is the only source of wealth, and that the wish to augment our fortunes and to rise in the world – a wish that comes with us from the womb, and never leaves us till we go into the grave – is the cause of wealth being saved and accumulated: he has shown that labor is productive of wealth when employed in manufactures and commerce, as well as when it is employed in the cultivation of the land; he has traced the various means by which labor may be rendered most effective; and has given a most admirable analysis and exposition of the prodigious addition made to its powers by its division among different individuals and countries, and by the employment of accumulated wealth, or capital, in industrious undertakings. He has also shown, in opposition to the commonly received opinions of the merchants, politicians, and statesmen of his time, that wealth does not consist in the abundance of gold and silver, but enjoyments of human life; that it is in every case sound policy to leave individuals to pursue their own interest in their own way; that in prosecuting branches of industry advantageous to themselves, they necessarily prosecute such as are, at the same time, advantageous to the public; and that every regulation intended to force industry into particular channels, or to determine the species of commercial intercourse to be carried on between countries, is impolitic and pernicious – injurious to the rights of individuals – and adverse to the progress of real opulence and lasting prosperity.

J. R. McCulloch, on Adam Smith and Laissez-Faire from The Principles of Political Economy, 1830. Reprinted

in: Charles Dickens, Hard Times. W.W. Norton & Co, 1990: 318-319.

The text leads us to conclude that:

Item 0 - Merchants, politicians, and statesmen in Smith’s time shared the idea that precious metals were what wealth was all about.

Provas

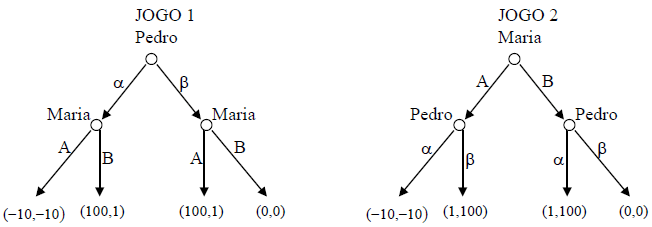

Considere os jogos na forma extensiva apresentados a seguir.

Item 1 - No jogo 1, a estratégia !$ \alpha !$ é dominante para Pedro.

Provas

BASED ON YOUR INTERPRETATION OF THE TEXT THAT FOLLOWS, DETERMINE IF EVERY STATEMENT IS RIGHT OR WRONG.

THIRD TEXT

As dramatic as it was, the global financial crises of 1997-99 was only the most recent of a rash of crises that have devastated market economies over the last 25 years. By one calculation almost 100 countries experienced a severe currency or financial crisis during that period, with adverse consequences for their national budgets and economic growth. Such patterns clearly call for an explanation: although there has been no dearth of suggestions, a consensus is growing that at least part of the explanation lies in weak financial institutions, which result in part from inadequate government regulation. The pendulum has come full circle: from the burst of enthusiasm over deregulation, policymakers now appreciate why it is that the most successful economies have long had a strong tradition of financial regulation. In the Unites States financial regulation dates back to 1863, in the middle of the American Civil War, when it became apparent that a strong banking system was essential to create a new national economy and that such a system required a strong national regulatory structure. The most recent major lapse in regulation, the deregulation effort that began in 1981, led to the savings and loan debacle. The consequences of that crisis were so severe that the U.S. economy did not recover for close to a decade.

But many developing countries are struggling with precisely the opposite problem – an overregulated financial system that stifles innovation and the flow of credit to new entrepreneurs, stunting the growth of even well-established firms. One of the many adverse effects of the East Asian financial crisis is that countries have become wary of reforms that affect the financial sector, aware that they may leave the country worse off. This article argues that reforms are possible – and indeed needed – and can be undertaken without undue fear, but success requires understanding the basic principles of financial sector regulation. The article sets forth those principles.

Even before the crisis, a theoretical literature argued that the nature of financial market failures necessitated a strong role for government. Failures in the banking system have strong spillovers, or externalities, that reach well beyond the individuals and firms directly involved. To avoid a financial collapse, governments typically bail out the affected entity, whether or not formal deposit insurance is in place; this intervention itself gives rise to problems of moral hazard. Although the absence of formal deposit insurance might give depositors a slightly increased incentive to monitor financial institutions (because there is some uncertainty about whether they will actually be bailed out), individual monitoring is actually inefficient. Monitoring is a public good, and it needs to be publicly provided. Of course, at a more practical level, a small depositor cannot be expected to examine the books of a bank on a weekly basis; there is strong evidence that regulators and rating agencies have difficulties doing so. Indeed, the widespread misconceptions about the appropriate strategy for regulating the financial sector suggests that even so-called experts are not fully aware of some of the key issues. Why, then, should one expect more from an individual depositor with little training, interest, or capacity in the arcane details of financial accounting?

Despite its long history, financial market regulation is poorly understood, as evidenced by the disasters associate with deregulation in industrial and developing countries. Often such measures were pushed through a burst of enthusiasm for free markets without recognizing the inherent market failures associate with such markets. Today few economists advocate unregulated banking, but a similar ideological agenda has pushed excessive reliance on a single regulatory instrument – capital adequacy standards. The belief is that this measure entails the minimal interference with the workings of the market and avoids the well-recognized problems of unregulated banks. A deeper analysis of the financial sector, however, shows that such reliance is not only inefficient but may even be counterproductive under some circumstances.

Principles of Financial Regulation: A Dynamic Portfolio Approach. Joseph E. Stiglitz. The World Bank

Research Observer, vol. 16, nº 1, Spring 2001.

According to the text:

Item 3 - The policy of bailing out of busted up banks may stimulate illicit behavior.

Provas

A evolução da economia brasileira na década de 1950 e até meados dos anos 1960 foi marcada por modificações profundas na política cambial, e cada uma dessas alterações constitui um marco decisivo no processo de desenvolvimento econômico. Assim, é correto afirmar:

Item 2 - A Instrução 113 da SUMOC, de janeiro de 1955, autorizou a emissão de licenças para importar sem cobertura cambial.

Provas

Caderno Container